The Crop Report

Case Study: $1 million portfolio Through 2000 - 2012

To demonstrate a guardrail strategy, we modeled a $1 million portfolio of stocks and bonds invested during a difficult period starting in January 2000, before the Dot-Com bust, through the Great Financial Crisis (2008–2009), with withdrawals adjusted for 3% annual inflation.

Disclaimer: Past performance is not indicative of future results. The $1M case study reflects historical data from 2000–2009; actual results vary based on individual factors like risk tolerance, fees, and market conditions.

This graph displays the period from 2000 to 2012, showing how long it took for a $1 million portfolio to break even after adjusting for inflation. By 2009, the portfolio following the 4% Rule with guardrail remained resilient, supporting long-term goals. This flexibility improves the ability to withstand market storms, taxes, and inflation.

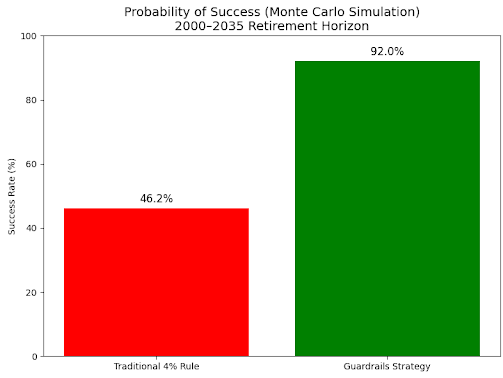

Longevity and Sustainability of Withdrawals

Now that we understand how these different approaches perform in adverse markets, what is the longevity and sustainability of these portfolios over 35 years? If we assume a person is 60 and lives until age 95, will they outlive their money?

Here is a graph showing the probability of Success Rate over a 35-year horizon for each strategy, using a Monte Carlo simulation, a computer-based method that employs repeated random sampling to model different outcomes.

Success ratio: % of 10,000 Monte Carlo simulations where a 60/40 portfolio lasts 30 years using 4% initial withdrawal (inflation-adjusted). Past performance is not indicative of future results.

Monte Carlo Success Rate: percentage of over 1,000 random scenarios where your plan never runs out of money.

- 4% Rule: 46% success (works in 460, fails in 540).

- Guardrails: 92% success (works in 920, fails in 80).

92% is strong—but many focus on the 8% failure (running out in 80 scenarios). How can you protect against that 8%?