The Crop Report 1

A Hypothetical Roth Conversion Scenario

Consider a hypothetical 60-year-old retired couple filing jointly with a $1,000,000 IRA Rollover and $238,000 annual retirement income.

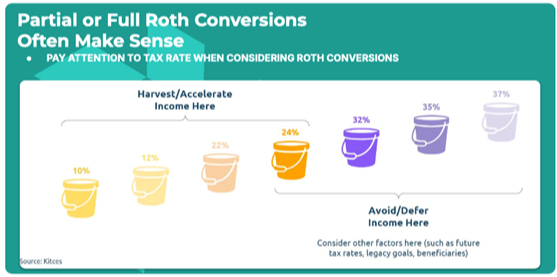

- After $30,000 standard deduction → $208,000 taxable income

- In 2025, the top of the 24% bracket is $383,900

→ $175,900 of “room” to convert to Roth without entering a higher bracket.

Why Convert $175,900/year?

- Lowers future Required Minimum Distributions (RMDs)

- Helps control taxable income in retirement

- May reduce Medicare premiums

- Moves assets into a tax-free Roth account

Long-Term Benefit (by Age 85)

- Traditional IRA: ~$8.2 million (after tax)

- Roth IRA (converted annually): ~$9.1 million (tax-free)

- Net advantage: + $885,000

Over time, this “bracket-filling” strategy can yield significant savings. In the above hypothetical, by age 85, it could result in a $9.1 million tax-free value, compared to $8.2 million after taxes in a traditional IRA—a $885,376 advantage.

This hypothetical is for illustrative purposes only and not a guarantee of results. Actual outcomes depend on individual circumstances and market conditions. This information is for educational purposes only and does not constitute financial advice or a guarantee of future results. The hypothetical example of a $9.1 million tax-free value versus $8.2 million after taxes, resulting in a $885,376 advantage, is based on specific assumptions (e.g., tax rates, investment growth, and longevity) that may not apply to your individual circumstances. Performance and savings are not guaranteed, and actual outcomes may vary due to market conditions, tax law changes, and personal factors such as age, income, and investment choices. Consult a qualified financial advisor or tax professional to assess the suitability of Roth IRA conversions, especially at a 37% marginal tax bracket or for strategies involving undervalued assets, long-term tax control, or legacy goals. Past performance is not indicative of future results.

In summary, Roth conversions support proactive tax planning, helping you manage future liabilities, preserve wealth, and optimize retirement income. However, complexities like non-deductible IRA contributions require careful attention. A personalized analysis—considering tax brackets, age, income, RMDs, and market conditions—is crucial.

Consult a tax professional to understand the tax implications and avoid pitfalls. Our team is here to analyze your unique situation and explore options.

Which strategy is best for your family, and how much should you consider?

The investment foundation of these strategies is high-quality, short-term bonds. Since the expected returns of bonds are low, use as few as possible and as many as necessary. The dollar amount needed depends on your spending habits and life priorities. Below, we’ll provide a few examples based on typical life stages (“learn it, earn it, burn it”).

Wealthy Household: An essential spending approach with a complementary 2-year protective reserve. An inflation-protected fixed income portfolio is matched dollar for dollar to cover the total essential spending needs for the rest of your life. The protective reserve enables spending and an additional self-insurance portfolio to handle unexpected emergencies or recessions.

Early career households have high spending flexibility and rely heavily on future earnings, making career development their most valuable financial asset. A 1.5-year protective reserve, disability, and life insurance (if children are present) help safeguard against income loss. Build a protective reserve first, then invest in risk assets.

Transitioning Household (approaching retirement), essential spending is NOT protected, and a 5-year protective reserve is necessary to cover core spending needs. This five-year reserve acts as a risk mitigation strategy against “sequence risk,” which involves poor investment returns or market downturns near retirement that can reduce your portfolio's value at the worst possible time.

Retired Household: Essential spending is protected, and a complementary 3-year protective reserve helps offset unexpected expenses, such as health-related expenses.

Wealth is often permanently destroyed when risk assets are sold at market bottoms during recessions or market corrections to meet immediate cash needs. Optimizing the "right" amount of cash and bonds as a protective strategy is a safety net, helping you weather acute and long-term financial storms by covering unexpected expenses and sustained challenges.

Click to schedule a call with the Harvester Wealth Team